- Published on

About 6 months ago, we invited our trusted partner and mortgage professional, Scott Bothel of North Pacific Mortgage, to write a guest post for us to share his thoughts on the state of mortgage interest and what it meant for us. Well, he's back with an update with his own blog post and we asked for permission to share it with you. Here it is in its entirety.

Since January of 2022, conventional mortgage rates have been rising at a pace that has derailed the home purchase plans of many Americans. With increased rates, come increased monthly costs and a decrease in the value of home you can qualify for purchasing. This has made a huge impact on the real estate market and the popular opinion of the affordability of buying a home.

Despite these increases, many families and individuals still understand the value of owning a home and are making plans to purchase in the coming years. But every savvy potential buyer is asking where are rates going? If rates are going to come back down, does it make sense to buy now or hold off? With that question in mind, I want to provide you some perspective on the potential movements of mortgage rates in the near future.

Please note, these are just opinions and should not be construed as direct financial advice. Always make sound decisions regarding your personal situation with a trusted professional.

I Remember When…

If you happen to be older than about 55 years old, you might wondering what all of the fuss is about. Rates for purchasing a home in the early to mid 1980’s topped 18%, making it quite painful to find and qualify for a home for many folks. This was the result of some unstable banking conditions in those years and luckily started to wind down by the middle of the decade. These rates were not typical and more importantly, local real estate and income trends tend to make it difficult to make direct comparisons when you’re trying to buy a home.

We aren’t headed back to the 1980’s due to major changes in the stock market, securities, and monetary policy, so where are we headed? Below are several snapshots of interest rates on conventional 30 years mortgages for some perspective.

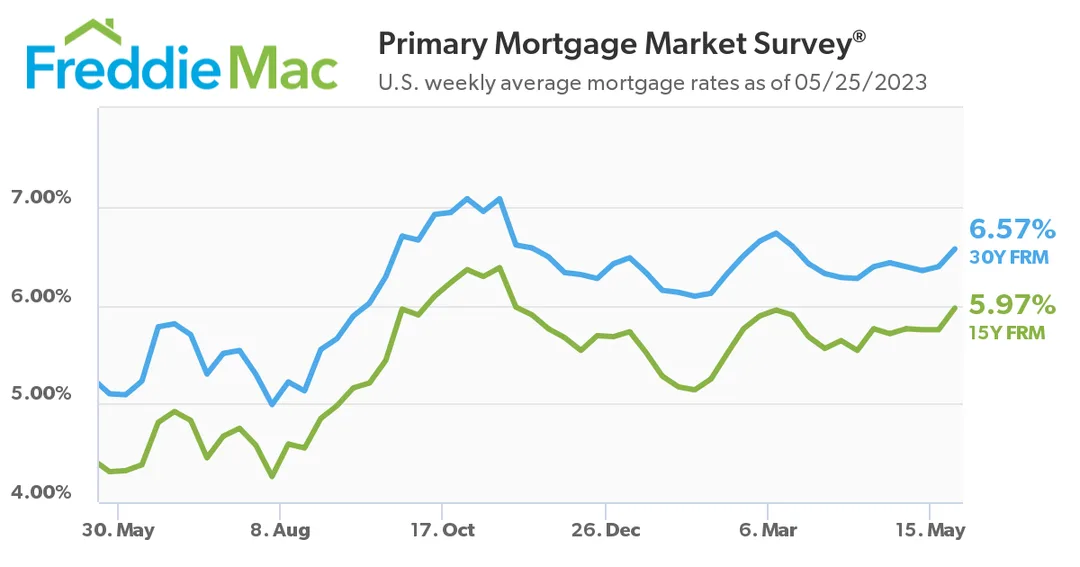

1 Year View

Despite these increases, many families and individuals still understand the value of owning a home and are making plans to purchase in the coming years. But every savvy potential buyer is asking where are rates going? If rates are going to come back down, does it make sense to buy now or hold off? With that question in mind, I want to provide you some perspective on the potential movements of mortgage rates in the near future.

Please note, these are just opinions and should not be construed as direct financial advice. Always make sound decisions regarding your personal situation with a trusted professional.

I Remember When…

If you happen to be older than about 55 years old, you might wondering what all of the fuss is about. Rates for purchasing a home in the early to mid 1980’s topped 18%, making it quite painful to find and qualify for a home for many folks. This was the result of some unstable banking conditions in those years and luckily started to wind down by the middle of the decade. These rates were not typical and more importantly, local real estate and income trends tend to make it difficult to make direct comparisons when you’re trying to buy a home.

We aren’t headed back to the 1980’s due to major changes in the stock market, securities, and monetary policy, so where are we headed? Below are several snapshots of interest rates on conventional 30 years mortgages for some perspective.

1 Year View

This one-year perspective shows us the continued rising rates culminating in highs over 7% in November of 2022. This has been fueled by significant inflation and the governments response to attempt to limit it. It’s important to note that the government does not directly control these rates, but they are determined by the value of mortgage backed securities on the secondary bond market. So anticipation of government action can impact rates just as much as actual actions.

Many experts see the current actions of the Fed as having sufficient impact on inflation that rates are likely to trend downward in the coming months. The recent debt limit standoff presented some struggles to seeing the decline begin, but with resolution, we are already seeing improvements coming.

5 Year View

Many experts see the current actions of the Fed as having sufficient impact on inflation that rates are likely to trend downward in the coming months. The recent debt limit standoff presented some struggles to seeing the decline begin, but with resolution, we are already seeing improvements coming.

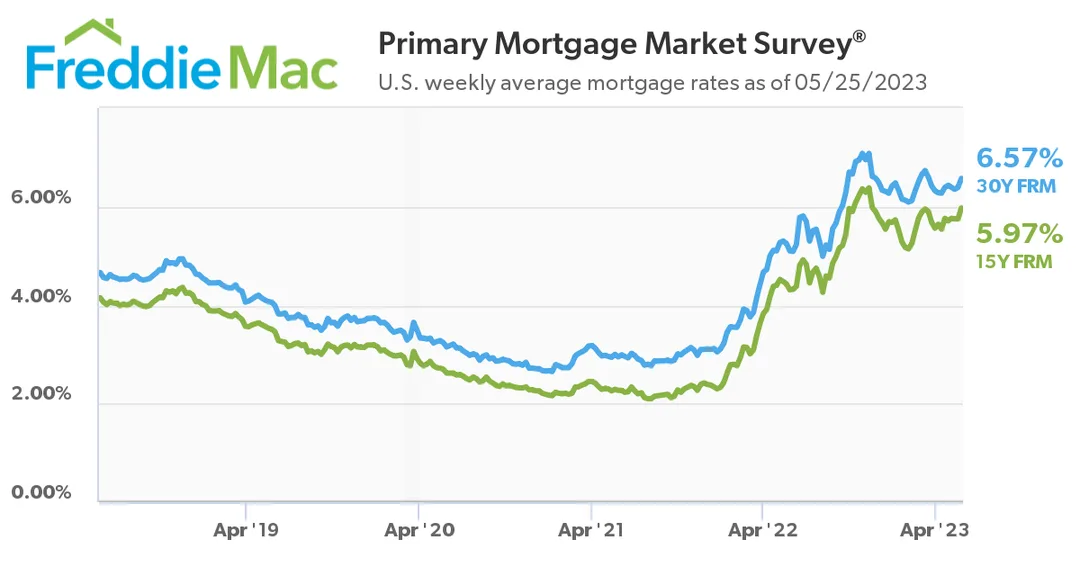

5 Year View

The five year view gives a more jarring picture of recent increases and fuels concerns by many potential homebuyers that affordability might still be a long way off in the real estate market. A major factor in the current real estate market is the reality that as rates reached record lows from 2012 to 2021, many homeowners refinanced their existing mortgages and now have rates below 4%. That means that if they choose to move, they will end up not being able to afford the same house for the same price due to the impact of today’s higher rates. This is a powerful force in deciding whether or not to sell you current home.

The Wide View

The Wide View

So, should we expect rates to come back down near 2% if we just wait long enough. Not likely. This is an important concept to see illustrated, so I created a specialized view with an overlay of recessions and impacts from Fed actions known as Quantitative Easing. Quantitative Easing, or QE as it is referred to in shorthand, is a policy of the US government to purchase trillions of dollars in Mortgage Backed Securities on the secondary market in order to prop up the value of bonds and stimulate the issuing of home loans. All of that served to create much lower rates than the market would have normally produced.

In the above graphic, you will notice periods of QE lead directly to the lowering of rates. Of course these were in reaction to recessionary movements in the economy, but many suggest the period of very low rates we experienced were only a result of the Fed extending their QE actions longer than necessary. The impact of QE and direct COVID relief payments was to inject a huge amount of cash into the economy and lower the cost of lending to record lows.

Where and When?

So, where are rates likely to land and when will they get there? I am not able to see the future, but here are some guidelines to consider. #1 Getting below 4% would likely require government actions. It is not likely that a return to normal market forces will result in rates much lower than 5%. These would still be considered historically appropriate levels despite anyone below 40 years of age feeling like they are out of whack.

#2 The timing of movements are impacted back a very complex number of factors. The price of oil, the rate of decline of inflation, wars in Ukraine and Sudan, banking crises, and elections can all impact the timing of a return to ‘normal.’ There is likely to be more slowing of the economy and pain in the job market before rates come down significantly. And if those things don’t occur, the Fed is likely to keep their foot on the gas of raising the Fed Funds Rate.

So, When is the Right Time to Buy?

All of these factors come together to paint a picture of caution. Major choices like a home purchase, should only be made when you’re in a position being confident in your ability to cover the costs of borrowing. A home should not be purchased with a built-in assumption of either dropping rates OR rising home values. Yes, you can refinance when rates go down, but no one can tell you when that might be.

The best path forward is to make a plan that works for you and your family according to your existing known circumstances. Need help figuring out what that means? Let’s chat.

In the above graphic, you will notice periods of QE lead directly to the lowering of rates. Of course these were in reaction to recessionary movements in the economy, but many suggest the period of very low rates we experienced were only a result of the Fed extending their QE actions longer than necessary. The impact of QE and direct COVID relief payments was to inject a huge amount of cash into the economy and lower the cost of lending to record lows.

Where and When?

So, where are rates likely to land and when will they get there? I am not able to see the future, but here are some guidelines to consider. #1 Getting below 4% would likely require government actions. It is not likely that a return to normal market forces will result in rates much lower than 5%. These would still be considered historically appropriate levels despite anyone below 40 years of age feeling like they are out of whack.

#2 The timing of movements are impacted back a very complex number of factors. The price of oil, the rate of decline of inflation, wars in Ukraine and Sudan, banking crises, and elections can all impact the timing of a return to ‘normal.’ There is likely to be more slowing of the economy and pain in the job market before rates come down significantly. And if those things don’t occur, the Fed is likely to keep their foot on the gas of raising the Fed Funds Rate.

So, When is the Right Time to Buy?

All of these factors come together to paint a picture of caution. Major choices like a home purchase, should only be made when you’re in a position being confident in your ability to cover the costs of borrowing. A home should not be purchased with a built-in assumption of either dropping rates OR rising home values. Yes, you can refinance when rates go down, but no one can tell you when that might be.

The best path forward is to make a plan that works for you and your family according to your existing known circumstances. Need help figuring out what that means? Let’s chat.

Scott is a Northwest native with a long history in the local business community. Having been raised in a Real Estate household, his passion has always been helping people achieve their goals by stewarding their greatest assets well. He focuses on low-pressure and high-empathy home loan process that ensures each client feels empowered and educated. He and his wife and three boys live in Bothell, Washington and they enjoy the confusion their last name creates. Their family is deeply committed to serving vulnerable people in their local and global community. He can be reached at scottb@npacificmortgage.com.

We do not provide legal or tax advice. You should consult their own legal or tax advisor. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

0 Comments