|

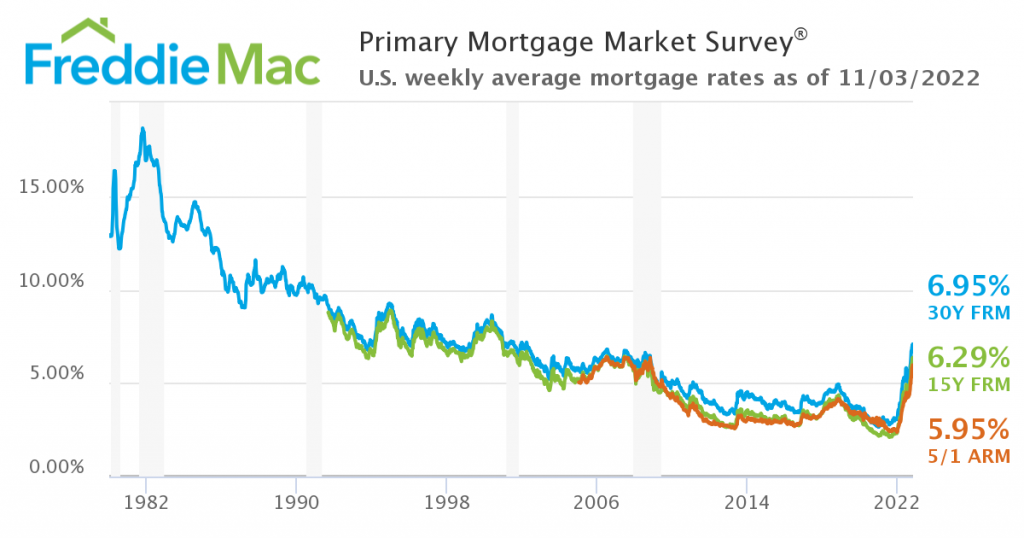

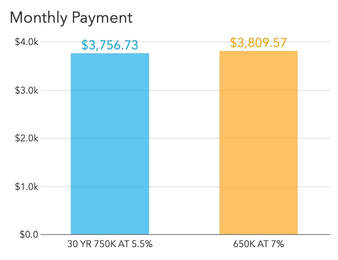

It’s hard to believe, but it was only a year ago when a 30-year fixed mortgage rate was around 3%. The sudden and rapid rise of the rate has been unnerving for homebuyers and sellers (and observers) alike. What are we to make of it? Well, we are grateful for our trusted partner and mortgage professional, Scott Bothel of North Pacific Mortgage, for his insight and thoughtful explanation on today’s mortgage environment and what it means for us.  If you are a homeowner or are trying to buy into the real estate market for the first time, it's likely that you are wondering what is happening with interest rates. As interest rates rushed from 3% to recent highs around 7%, we were left wondering what's going on and how should we respond. Whether you are an investor, first-time buyer, or are forced into a move by relocation, the idea of taking such high rates feels like a very bitter pill. Let's put these rates in perspective and ask, what now? Why have mortgage rates risen? Despite all of the talk about the Federal Reserve Board "raising rates" this year, the Fed actually does not control mortgage rates. Mortgage rates are determined by the value of Mortgage Backed Securities which are sold on the market as bonds. What the Fed has done is increase the underlying cost to borrow money in an effort to cool off the speed of the economy and hopefully, slow down the current rate of inflation which is causing all sorts of disruptions to consumers and businesses alike. As institutional investors seek higher returns for their money in order to keep their heads above the rate of inflation, government bonds must offer higher returns and those are the same investors mortgage banks are courting for their new loans. To make those more attractive, mortgage banks must raise rates as well. If you want to work further back to understand the historic reasons for inflation and higher rates, you'll have to consider a lot of factors ranging from the Fed's Quantitative Easing policies after the last financial crises, the impact of COVID-19, and the war in Ukraine. Are mortgage rates of 7% normal? The word "unprecedented" has become a favorite in the media lately, but if we look at historic data on mortgage rates, we are not in uncharted territory. With many boomers remembering the mortgage rates topping out at almost 20% in the early 1980s, they chuckle hearing their children stressing out over our current numbers. Perspective is everything here, though. Rates haven't hit 7% since the year 2002, which may sound recent to you until you realize that was 20 years ago. There are new families needing housing that haven't ever known rates to be above 5.5% in their living memory. The hardest reality for these folks is the speed of increase on rates, leaving many excluded from the market due to the impact of rates on affordability. For these potential buyers, the current situation is unprecedented, indeed.  What can I do if I need to borrow in a high mortgage rate environment?So, what should you do? Answering this question ofter requires a combination of documenting your financial goals, working with a financial planner, your partner, and these days maybe even a relationships counselor. Talking about money can be hard, so it's important to frame your discussions around your priorities. Here are some factors that contribute.  Affordability - Higher rates directly impact how much house you can afford. In a recent discussion I looked at the impact of 1.5% rise in rates on a potential home purchase. A buyer who may have been approved last spring to buy a $750k home at a 5.5% rate, will now only qualify for a $650k home at a 7% rate. Simply buying less house might be what some are forced to consider. Time Frame - Other strategies to mitigate the impact of rates on affordability include paying points on a loan or using a temporary buy-down strategy. In both cases, you are putting more money down upfront in order to reduce the mortgage rate for either short-term (2-3 years) or long-term (5+ years) impact. Some expect to refinance any purchase made this year in the coming 2-3 years to take advantage of rates that are assumed to be coming down from their current levels. It's important to note that no one can predict the future and all of these decisions should be made with your particular risk factors and tolerance in mind. Leverage - Other buyers simply wonder if this is the right time to enter the market. If prices decrease, will I lose my investment? This is a very real concern for those who lived through the 2008 housing crisis. It's important to note that we are not seeing the same underlying problem with equity that impacted most distressed borrowers in that time-frame and that mortgage regulations since 2008 have drastically changed how buyers are approved for mortgage loans. With those things in mind, if the market continues in similar fashion to what it's done since the 2008 crisis, modest gains in a home investment can be a major stepping stone for the average family. This is due to the principle of leverage, that if you put 10% down on a home, and it increases by 5% in value in the coming year, you don't just see the benefit of your 10%, but instead you realize the full benefit of 5% on the total value of the home. Putting more money down also helps ensure you won't end up with a an equity crisis in the short-term. Conclusion It's important to remember in all of this that buying a home should match with your long-term goals for career and family. Families who bought in 2007 may have been upside down in their mortgage for a period of time, but if they maintained employment and continued to see that house as home, their long-term investment was protected. Make choices knowing the current rate environment will not stay the same, but make choices that whether the storms of uncertainty as they come. Scott is a Northwest native with a long history in the local business community. Having been raised in a Real Estate household, his passion has always been helping people achieve their goals by stewarding their greatest assets well. He focuses on low-pressure and high-empathy home loan process that ensures each client feels empowered and educated. He and his wife and three boys live in Bothell, Washington and they enjoy the confusion their last name creates. Their family is deeply committed to serving vulnerable people in their local and global community. He can be reached at [email protected]. We do not provide legal or tax advice. You should consult their own legal or tax advisor. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

Comments are closed.

|

|

Advisory services offered through CS Planning Corp, an SEC registered investment advisor.

Insurance products offered through Elliott Bay Insurance LLC. Form CRS, Privacy Policy, and Additional Disclosures. |