|

Look out. There’s a new payroll tax in town. The new mandatory state payroll tax in Washington state under The Long-Term Care Trust Act is designed to fund long-term care benefits for its eligible residents. If you are employed in Washington (or will be), read on or download our whitepaper below. This new tax will affect you.

HOW MUCH IS THE TAX? The tax rate is 0.58% of wages. For example, if your wages are $100,000 a year, your tax is $580 a year. At $200,000, the tax is $1,160, and so on. The first payroll deductions begin January 1, 2022. You might be curious if there’s a ceiling on the income subject to the payroll tax. Unfortunately, no, there isn’t. It doesn’t matter how much or how little you make. You’re taxed 0.58% on all of your wages. That means if you make $1,000,000, the whole amount is taxable. So your tax bill is $5,800. With a $10,000,000 paycheck, your tax would be, you guessed it, $58,000. The rate is set at 0.58% initially on January 1, 2022. Then it gets reset to 0.58% every two years starting on January 1, 2024. Between these reset dates, however, it’s possible that the rate will go up to maintain solvency of the Program. WHAT COUNTS AS INCOME? “Wages” under this Act is the so-called “W-2 income.” The obvious ones are salaries and bonuses. But wages also include other forms of remuneration like:

WHAT IF YOU'RE NOT A W-2 EMPLOYEE? Is your income subject to the payroll tax if you are self-employed, an independent contractor, a sole proprietor, or a partner in a partnership? The short answer is, no, your income is not taxable. But you may still opt in to be taxed. You have until January 1, 2025 to opt in. Or if you become self-employed for the first time after that date, you can opt in within 3 years of becoming self-employed. The decision is irrevocable, so once you opt in, there’s no turning back. WHAT IS THE BENEFIT? So what do you get in return for your contributions into the system? Here’s a quick rundown:

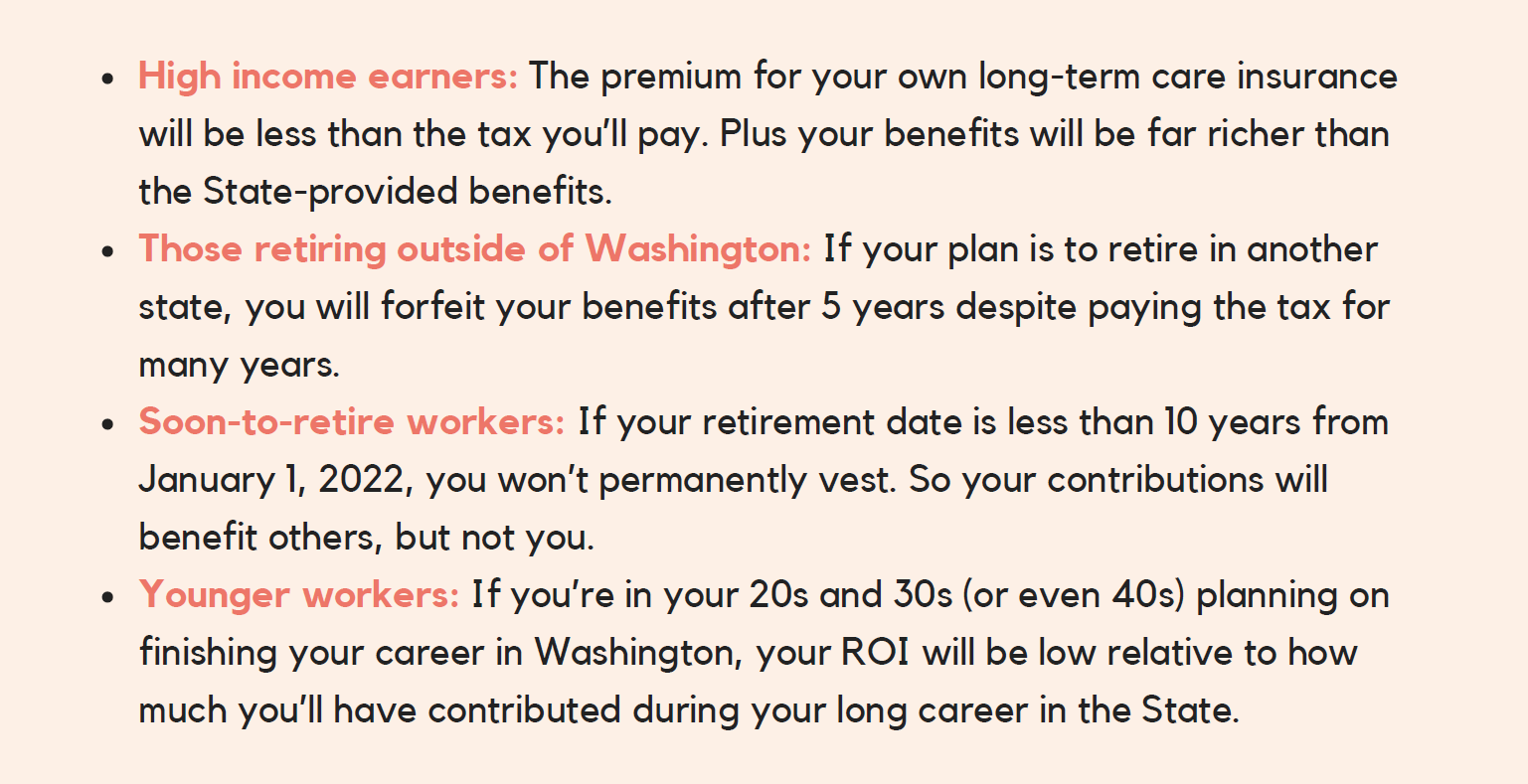

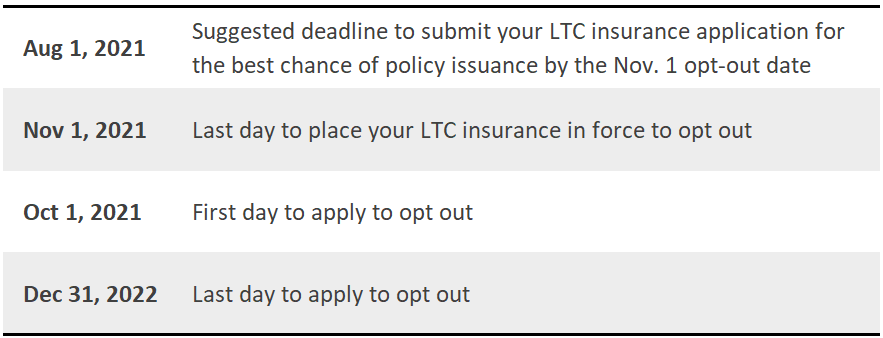

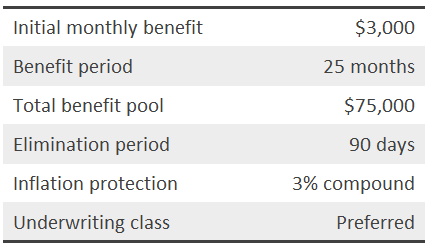

The benefits are the same for everyone. It doesn’t matter what your income was or how much you contributed. Everyone gets the same benefits. That means the coverage for someone who contributes $5,800 a year for 30 years is the same as a worker who contributes $290 a year for 12 years. Wait, but there’s more. Only Washington residents can qualify for benefits. If you move out of state for 5 or more years, you forfeit your benefits and the tax you paid during your working years in Washington state. To top it off, you have to vest to receive benefits. To permanently vest, you must work a minimum of 500 hours per year and pay the tax for at least 10 years without a break of 5 consecutive years. You can also vest on a temporary basis if you paid the tax for 3 years within the last 6 years from the date of application for benefits. So if you don’t apply for benefits within the first few years of retirement, you’ll eventually be unvested. HOW TO OPT OUT This payroll tax may not make sense if you are one of these people:  Fortunately, there’s a way to opt out of this tax. First, you must purchase your own long-term care insurance before November 1, 2021. Coverage must be in place by that date. This means that a pending, unapproved application will not count toward opting out. You should note that the application process can take several weeks to several months depending on your health, access to medical history and so forth. Likewise, we anticipate carriers will experience a huge backlog. We are asking our clients to submit their applications by August 1, 2021 to give themselves the best chance for policy issuance by November 1st. After your policy is in place (before the November 1, 2021 deadline), you must apply to opt out between October 1, 2021 and December 31, 2022.  Remember these important dates. If you miss them, you will forever be subject to the payroll tax for as long as you earn wages in Washington. LONG-TERM CARE INSURANCE: THE BASICS Perhaps you are interested in exploring getting your own long-term care coverage to opt out of the state program. We'll walk you through what exactly is involved in applying for and getting coverage. First, let's outline basic features of a long-term care insurance policy.  It's important to note that actual monthly costs of care in Washington state are substantially higher than $3,000. We chose the $3,000 monthly benefit here for illustrative purpose to approximate the state's $100 daily benefit. Now, let’s discuss the policy features in plain English:

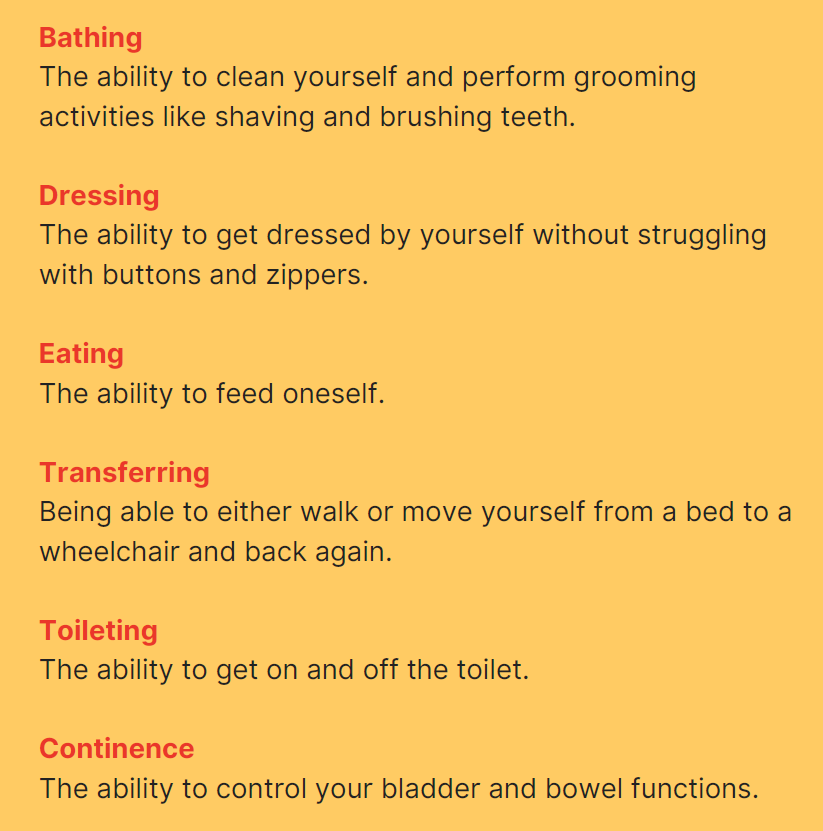

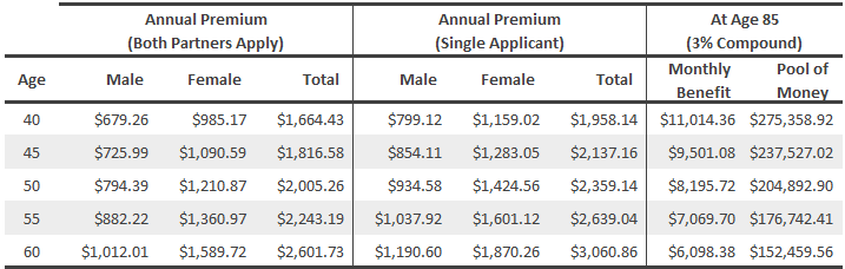

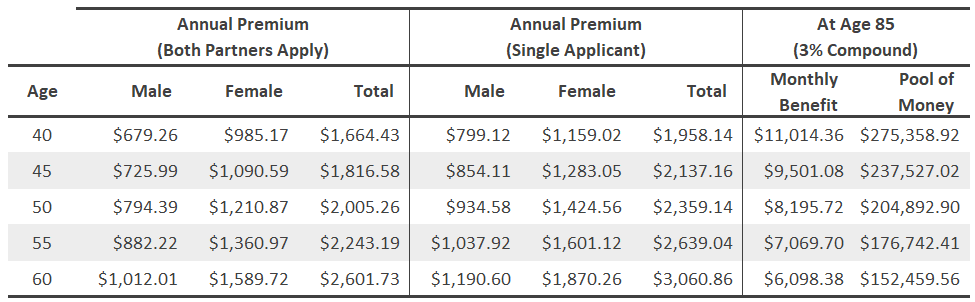

Your benefits generally trigger when you can’t perform 2 of 6 activities of daily living (ADLs) listed below:  Interestingly, the state program requires 3 out of 10 ADLs for benefit trigger. The 10 ADLs are: medication management, personal hygiene, eating, toileting, transferring, body care, bathing, ambulation/mobility, dressing, and cognitive impairment. HOW MUCH DOES INSURANCE COST? Now, let’s look at the rates for the same policy at various ages for nonsmokers in good health ("Preferred" rating). Again, this policy provides $3,000 monthly benefit for 25 months, growing at 3% with a 90-day elimination period.  As you can see, the younger you are, the lower the premium. And premiums for females are higher than those for males. Furthermore, a couple applying together gets a discount. Again, these rates are based on the Preferred underwriting class, which is for healthy individuals with clean medical history. Obviously, not everyone will qualify for Preferred, and there are additional underwriting classes. Right below Preferred is Select, and there are a couple more classes below Select. Premiums are cheapest for Preferred, and it goes up from there. So the healthier you are (in the insurance carrier's eyes), the cheaper the premium. Premiums are payable for life and can increase in the future. For those who want a shorter premium payment period and be done with it, there is a product that allows you to pay premium in one lump-sum or over 10 years. OTHER OPTIONS (NON-TRADITIONAL PRODUCTS) In addition to the traditional long-term care insurance we’ve discussed thus far, you have two other product options:

For younger applicants, instead of a stand-alone long-term care insurance that they might not need for perhaps a half century or more, they might consider life insurance with a long-term care rider. This way, they can get their life insurance coverage (which they often need anyway) and build cash value while opting out of the tax. Alternatively, as a part of their gifting strategy, parents can consider paying for life insurance with a long-term care rider for their children in their 20s and 30s. As for hybrid products, as the name might suggest, it’s a hybrid between long-term care and life insurance. Premium structures are often more flexible as you can pay in one lump-sum or over time. And unlike traditional long-term care insurance, premiums are guaranteed to never increase. Like life insurance, there is a small death benefit should you never use long-term care benefits. Similarly, there is also a cash value which you can recoup, subject to vesting, if you decide to cancel the policy in the future. UNDERWRITING The process of applying for long-term care insurance is itself relatively straightforward. In addition to paperwork, it generally involves only a phone interview and you typically won’t get a visit from a nurse for an exam. There are exceptions, however. For example, if you haven’t seen a doctor for the past 24 months, insurance company might require a paramedical exam with blood and urine samples. A phone interview involves asking questions about your medical history, but the interviewer is also trying to assess your cognitive functions as you interact with them. Underwriting for long-term care insurance is different from that for life insurance in that it evaluates one’s morbidity (vs. mortality for life insurance). Morbidity has to do with the state of being diseased or unhealthy. Think of fragility related to aging – high blood pressure, high cholesterol, extra pounds, arthritis, joint problems, cognitive decline, and so on. As we live longer, these health issues can become more pronounced and may lead to inability to perform some activities of daily living. As a matter of practice, we ask every applicant to complete a health prequalification form. This has helped minimize surprises and disappointments, and saved time for all involved parties. ACTUAL COSTS OF CARE Our focus so far has been on the new payroll tax and the ways to avoid it with long-term care insurance. But beyond the theoretical exercise of tax avoidance, what does it actually cost to get long-term care in Washington state? According to Genworth Costs of Care Survey, the 2020 median monthly costs of care for Washington state are:  Not surprisingly, costs of care are slightly higher for the Seattle area than the state as a whole. Statistics on long-term care are quite sobering. You can read more about it on the Morningstar website. Here's a sample.  FREQUENTLY ASKED QUESTIONS What if I get a policy, opt out of the tax, and then cancel it a few months later? The law does not address this question, but it’s clearly counter to its intent. So we'll say jokingly, “We’ll leave it up to your conscience.” The state will most certainly come up with anti-abuse rules to combat this loophole. What’s the minimum coverage I need to get to opt out? Again, the law is silent on this issue, but this is what we know so far. According to Long-Term Services and Supports Trust Commission of the Department of Social and Health Services, "there are no standards of equivalent coverage that have to be met." Similarly, the Employee Security Department stated, "there is no minimum requirement of coverage under RCW 50B.04.085 for private long term care insurance policies." For someone who wants a basic policy just to avoid the tax, we recommend $3,000 monthly benefit with 3% inflation protection to approximate state’s $100 daily benefit indexed with the CPI. I am an employer. Can I provide policies for my employees? You have two options:

Simplified issue bypasses traditional underwriting and uses a health questionnaire instead. Interestingly, the carrier will not make an offer under simplified issue if the ratio of female employees is more than 50%. The second option requires traditional underwriting as if you apply for your own coverage. You just get a “volume discount" for multiple people applying at once. NEXT STEPS As you can see, there are several moving parts and important deadlines. You get only one shot at opting out. For additional information and details, you can contact our team at Cultivant. We do not provide legal or tax advice. Readers should consult their own legal or tax advisor. There is no guarantee investment strategies will be successful. Investing involves risks, including possible loss of principal. There is always the risk that an investor may lose money. A long-term investment approach cannot guarantee a profit. Investors should talk to their financial advisor prior to making any investment decision. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

Comments are closed.

|

|||

|

Advisory services offered through CS Planning Corp, an SEC registered investment advisor.

Insurance products offered through Elliott Bay Insurance LLC. Form CRS, Privacy Policy, and Additional Disclosures. |