- Published on

Generally positive capital markets along with ample helpings of uncertainty have been the primary feature of this last quarter in the financial markets. A fair sprinkling of positive developments have continued to influence the bullish among us as inflation moderated, jobs remained plentiful, the debt ceiling standoff was resolved and folks contemplated the potential productivity enhancing attributes of many of the AI related technologies.

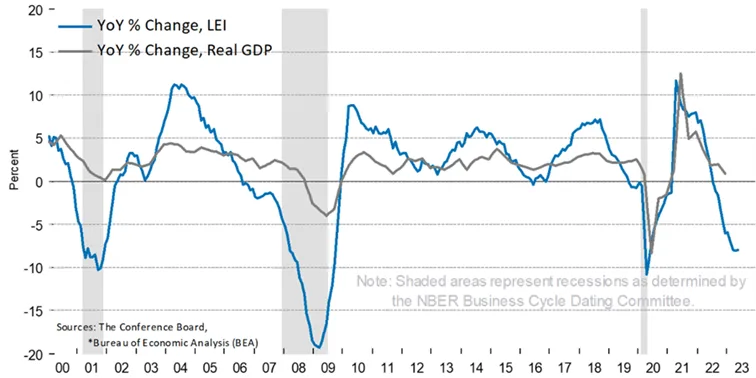

Bears however continued to find grist for their mill in the ongoing slide in the Leading Economic Indicator results (negative for the 14th month in a row), the narrowness of the equity markets (with most of the gains coming from the stocks of the very largest companies) and the potential for further hiking of rates by the Fed (after the pause in increases over the last month).

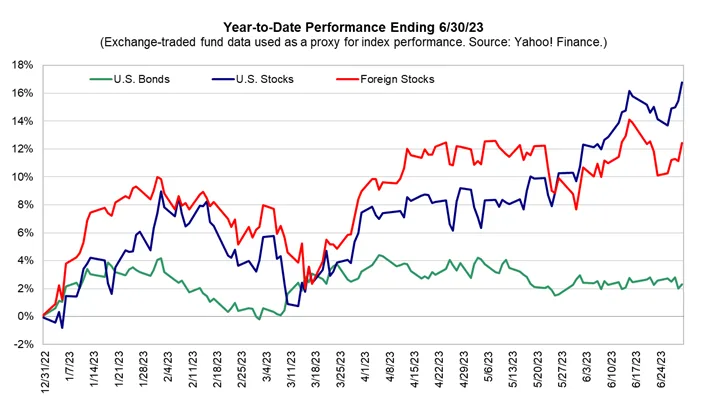

So far this year the bulls have been in the majority and both stock and bond markets have benefitted. The excitement about new developments in artificial intelligence has pushed up the valuations of many types of technology stocks and that in turn has been a catalyst to move the markets higher. While the market advance has been somewhat narrow, benefitting technology and large company stocks more than others, there have been signs of these advances broadening out of late.

So far this year the bulls have been in the majority and both stock and bond markets have benefitted. The excitement about new developments in artificial intelligence has pushed up the valuations of many types of technology stocks and that in turn has been a catalyst to move the markets higher. While the market advance has been somewhat narrow, benefitting technology and large company stocks more than others, there have been signs of these advances broadening out of late.

In addition to the advances due to the promise of AI the economy in general has been muddling along. GDP grew in the 1st quarter, improving by a respectable 2%. Inflation, while still higher than the Fed will tolerate, has slowed considerably year to date. Corporate earnings, while lower in the 1st quarter than the previous quarter (2nd quarter numbers have yet to be released) have so far slowed less than forecast. While the leading economic indicators (LEI) have been signaling the onset of a recession for some time, so far the economy has avoided that result. As we discussed last quarter it may be that we’ll get a softer landing than otherwise feared but only time will tell.

How do we as investors parse these differing viewpoints and provide ourselves with a sense of financial wellbeing in our always uncertain world? What are the risks we should be cognizant of as we try to make sense of the economic outlook and how to position our portfolios considering those?

Market risk is the first risk that most of us think of when we think about our portfolios. Markets can decline and that decline is very much visible on our account statements. Last year we saw that sort of risk in both stocks and bonds. Stocks fell on concerns of rising interest rates that might push the economy into recession and bonds fell due to those same rising rates. We have had a considerable rally so far this year in both stocks and bonds as investors feel that we are closer to the end of the rising rate environment and even look forward to a time when rates might fall.

Those recessionary fears we might anticipate from the LEI chart above could even be an indicator of a future market rally as so much of last year’s angst was due to rising rates that might lead to recession and a recession could very well mean the end of rising rates and the beginning of a period when rates would be trimmed to stimulate a weaker economy. Markets are always looking forward and trying to discern the next period so in this way a mild recession in our future could be seen as a benefit.

Market risk in equities can be managed to some degree but mostly it simply must be borne. The only way to sidestep it entirely is to be out of the market and periods like this year so far remind us that stock rallies (and declines) are quite unpredictable. Just as boats rise and fall with the tide so do markets and if you are in the water you must expect those fluctuations.

Market risk in our bond portfolio comes from two sources, rising interest rates which push down, at least temporarily, the value of many types of bonds and credit risk, the risk that certain types of bonds will fall in value because their credit worthiness changes. Interest rate risk, the result of which we saw in our portfolios last year, tends to diminish over time as the higher rates that negatively affect bond values also provide higher levels of dividend income that can be reinvested. Credit risk can also ebb and flow given the outlook for different sorts of bonds and is largely controlled through the portfolio design process, selecting credit qualities that are appropriate for the differing economic situations we find ourselves in.

There are other risks beside market and interest rate risk and managing them is fundamental to portfolio design and sound financial planning. As it is inextricably tied to our portfolio planning and design it is worth touching on inflation risk, a risk that we all but discounted through much of the last decade and which suddenly became much more real after last year. Rising prices over the last few years didn’t affect the value of our portfolio per se but certainly made a difference in the prices we paid for goods and services. Over time we can hedge away inflation risk in our portfolio by owning things, either the actual things themselves or, as a proxy, shares of companies whose pricing power will allow their profits to keep pace in an inflationary environment. We’ve seen this work in real time so far this year and, given time, it is the exposure to company shares in our portfolio that potentially helps us to keep level with inflation. It’s a good reminder of why we tolerate these pesky fluctuating equities in the first place!

Moving away from our risk discussion and back to the present state of our economy and the markets we’re guardedly optimistic about the future even as we realize there is a good chance for volatility as the year progresses. The actions of the Fed are designed to combat inflation and most of us realize that is a prescription for slowing growth. So far that slowing has been benign with the economy cooling at a measured pace.

Realistic expectations involve the probability of at least some sort of recessionary period in the next 6 to 12 months, although there is still a chance we’ll simply get to just above stall speed and muddle through from there.

From the standpoint of equities, we could see a pullback in technology issues and that could certainly have an influence on the broader market although, that said, much of the equity market remains reasonably valued having not participated as fully in this year’s gains. In the bond market most analysts don’t see large rate increases going forward even though some additional increases in rates on the short side are reasonable to assume given the current guidance from the Fed. As always, as discussed above, it is important to remember that markets are always forward looking and that the future, at this juncture, looks reasonably positive.

We continue to think it makes sense to remain diversified and we think diversification will be key in the months ahead, even while acknowledging that patience is a vital part of investment success.

Market risk is the first risk that most of us think of when we think about our portfolios. Markets can decline and that decline is very much visible on our account statements. Last year we saw that sort of risk in both stocks and bonds. Stocks fell on concerns of rising interest rates that might push the economy into recession and bonds fell due to those same rising rates. We have had a considerable rally so far this year in both stocks and bonds as investors feel that we are closer to the end of the rising rate environment and even look forward to a time when rates might fall.

Those recessionary fears we might anticipate from the LEI chart above could even be an indicator of a future market rally as so much of last year’s angst was due to rising rates that might lead to recession and a recession could very well mean the end of rising rates and the beginning of a period when rates would be trimmed to stimulate a weaker economy. Markets are always looking forward and trying to discern the next period so in this way a mild recession in our future could be seen as a benefit.

Market risk in equities can be managed to some degree but mostly it simply must be borne. The only way to sidestep it entirely is to be out of the market and periods like this year so far remind us that stock rallies (and declines) are quite unpredictable. Just as boats rise and fall with the tide so do markets and if you are in the water you must expect those fluctuations.

Market risk in our bond portfolio comes from two sources, rising interest rates which push down, at least temporarily, the value of many types of bonds and credit risk, the risk that certain types of bonds will fall in value because their credit worthiness changes. Interest rate risk, the result of which we saw in our portfolios last year, tends to diminish over time as the higher rates that negatively affect bond values also provide higher levels of dividend income that can be reinvested. Credit risk can also ebb and flow given the outlook for different sorts of bonds and is largely controlled through the portfolio design process, selecting credit qualities that are appropriate for the differing economic situations we find ourselves in.

There are other risks beside market and interest rate risk and managing them is fundamental to portfolio design and sound financial planning. As it is inextricably tied to our portfolio planning and design it is worth touching on inflation risk, a risk that we all but discounted through much of the last decade and which suddenly became much more real after last year. Rising prices over the last few years didn’t affect the value of our portfolio per se but certainly made a difference in the prices we paid for goods and services. Over time we can hedge away inflation risk in our portfolio by owning things, either the actual things themselves or, as a proxy, shares of companies whose pricing power will allow their profits to keep pace in an inflationary environment. We’ve seen this work in real time so far this year and, given time, it is the exposure to company shares in our portfolio that potentially helps us to keep level with inflation. It’s a good reminder of why we tolerate these pesky fluctuating equities in the first place!

Moving away from our risk discussion and back to the present state of our economy and the markets we’re guardedly optimistic about the future even as we realize there is a good chance for volatility as the year progresses. The actions of the Fed are designed to combat inflation and most of us realize that is a prescription for slowing growth. So far that slowing has been benign with the economy cooling at a measured pace.

Realistic expectations involve the probability of at least some sort of recessionary period in the next 6 to 12 months, although there is still a chance we’ll simply get to just above stall speed and muddle through from there.

From the standpoint of equities, we could see a pullback in technology issues and that could certainly have an influence on the broader market although, that said, much of the equity market remains reasonably valued having not participated as fully in this year’s gains. In the bond market most analysts don’t see large rate increases going forward even though some additional increases in rates on the short side are reasonable to assume given the current guidance from the Fed. As always, as discussed above, it is important to remember that markets are always forward looking and that the future, at this juncture, looks reasonably positive.

We continue to think it makes sense to remain diversified and we think diversification will be key in the months ahead, even while acknowledging that patience is a vital part of investment success.

This market commentary is provided for information purposes only and is not a complete description or analysis of the securities, markets or developments referred to in this material. There is no guarantee that these statements, opinions or forecasts provided will prove to be correct. All expressions of opinion are subject to change. Information has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance does not guarantee future results.

0 Comments