- Published on

It’s summer, the masks are mostly off, the economy is growing, and the sun is shining. Some of you might not remember Jackie Gleason’s line but somehow it seems fitting right about now. How sweet it is!

We’re not out of the woods quite yet but we’re sure close. This last quarter built on the prior one with expanding corporate profits, a continued increase in the job market and a significant degree of normalization of everyday living. Business leaders and investors both continued to look ahead with optimism about the prospects for even more improvement in the year ahead.

The final review of US GDP growth in the first quarter came in unchanged at a brisk 6% according to the Bureau of Economic Analysis. Estimates for Q2 have solidified, with the New York Fed GDP Nowcast currently calling for 3.4%, while the Atlanta Fed GDPNow is predicting 8.3%—both down a bit from recent weeks. Private forecasts from a variety of Wall Street firms have been ranging from 8.0% to 10.0%. Third-quarter estimates are beginning, with the New York Fed at 4.1%. The recovery in economic growth appears to be peaking right around now, although we could likely see above-average growth results for the balance of this year, and into at least early 2022.

Markets have anticipated these rates of recovery for some time and so it’s likely that these numbers are already accounted for in equity prices. Nonetheless this solid showing continues to reassure folks that economic growth will continue over the near and intermediate term and that growth in earnings will likely continue, even if at a slower pace overall as the recovery lengthens.

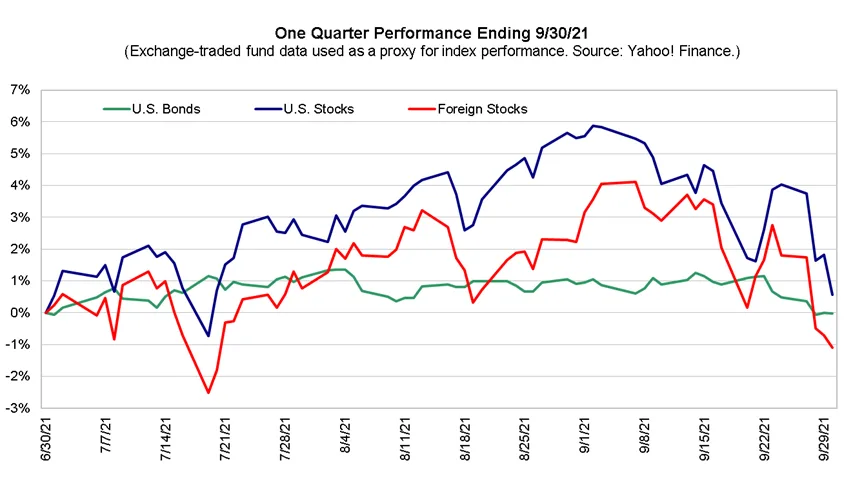

Have stocks gotten ahead of themselves? Valuation measures such as price to earnings and price to sales are near the high end of their historical range while other measures paint a more nuanced view. Most folks would tend to agree that stocks are not cheap by most measure. We saw some volatility in equity prices in May and June to do with the potential for higher inflation and we would expect more of the same (for a variety of potential reasons) as the year progresses.

Bulls and bears see different things as they gaze at the financial landscape. The bullish see the economy growing into these larger valuations as the recovery progresses, thereby bringing overall valuation measures back toward the average. The more bearish might instead consider the potential for a drop in prices to move those valuations lower. At this stage in the recovery, we could certainly see a bit of both as the prospects for continued growth seem reasonable to assume and volatility happens regularly over time.

Valuations are lower in markets outside of the US. The US economy has been rebounding very rapidly and so stocks here are priced for that robust growth. Overseas there are many firms with excellent growth prospects but not priced in the same manner as domestic companies.

Long term it is always about the economy. Longer term the equity part of our portfolio is there to grow with the economy over multiple periods of expansion and contraction. Equities are by nature a longer-term affair. Bonds and cash are the portfolio components we look to for more consistency and lower volatility. We don’t, for the most part, want all our eggs in one basket and portfolio diversification makes sure that doesn’t happen.

There is much to be cheerful about in the here and now. The stimulus measures have unleashed a flood of money to businesses and individuals and those dollars have been spent on all sorts of things, boosting the economy overall. There is potentially more stimulus of sorts on the way in the form of an infrastructure plan and other initiatives regarding education, health care and other domestic policy spending. Interest rates are remaining stubbornly low, even in the face of short-term inflation concerns. Tax policy is unlikely to change significantly over this year and next with our evenly divided Senate and all these pieces together create a very accommodative monetary and fiscal environment.

There are challenges too. Inflation could remain more persistent than economists suspect and erode some of the advantages of growth. Inflation has been very much on investors’ minds of late and, at some point, bond markets could react with higher interest rates, creating a headwind for the economy with increased costs for business and consumer purchases. There is still uncertainty about the trajectory of the virus and will be until most of the world’s population has been vaccinated. There is always plenty to worry about.

Times like these are excellent opportunities to review overall portfolio mix and contemplate the effect of volatility on our portfolios. While we don’t recommend trying to time the market, thinking about how our portfolio will react in the next downturn is a very useful exercise. Stocks are volatile, that is why we think of them as long-term investments. Over market cycles they tend to provide returns higher than those to be found in more conservative investments but over shorter periods their volatility can be discouraging to some. If we prepare for the inevitable downturn, we won’t be surprised when it appears, and that preparation will enable us to stick with our plan instead of allowing fear to precipitate costly mistakes.

Fortunately, we have a very recent example in the selloff of February and March of 2020. A quick review of your statements from that period will give a good idea of how your portfolio reacted then. Of course, not all downturns are alike, and the depth of the decline can vary. We’re certainly happy to discuss this with you at any time, just let us know.

In the meantime though, it’s summer, you can take your mask off (at least some of the time) and can enjoy those special times with family and friends that you may have had to put off for far too long. The economy is growing, and folks are going back to work. The sun is shining, and the birds are singing. How sweet it is!

Markets have anticipated these rates of recovery for some time and so it’s likely that these numbers are already accounted for in equity prices. Nonetheless this solid showing continues to reassure folks that economic growth will continue over the near and intermediate term and that growth in earnings will likely continue, even if at a slower pace overall as the recovery lengthens.

Have stocks gotten ahead of themselves? Valuation measures such as price to earnings and price to sales are near the high end of their historical range while other measures paint a more nuanced view. Most folks would tend to agree that stocks are not cheap by most measure. We saw some volatility in equity prices in May and June to do with the potential for higher inflation and we would expect more of the same (for a variety of potential reasons) as the year progresses.

Bulls and bears see different things as they gaze at the financial landscape. The bullish see the economy growing into these larger valuations as the recovery progresses, thereby bringing overall valuation measures back toward the average. The more bearish might instead consider the potential for a drop in prices to move those valuations lower. At this stage in the recovery, we could certainly see a bit of both as the prospects for continued growth seem reasonable to assume and volatility happens regularly over time.

Valuations are lower in markets outside of the US. The US economy has been rebounding very rapidly and so stocks here are priced for that robust growth. Overseas there are many firms with excellent growth prospects but not priced in the same manner as domestic companies.

Long term it is always about the economy. Longer term the equity part of our portfolio is there to grow with the economy over multiple periods of expansion and contraction. Equities are by nature a longer-term affair. Bonds and cash are the portfolio components we look to for more consistency and lower volatility. We don’t, for the most part, want all our eggs in one basket and portfolio diversification makes sure that doesn’t happen.

There is much to be cheerful about in the here and now. The stimulus measures have unleashed a flood of money to businesses and individuals and those dollars have been spent on all sorts of things, boosting the economy overall. There is potentially more stimulus of sorts on the way in the form of an infrastructure plan and other initiatives regarding education, health care and other domestic policy spending. Interest rates are remaining stubbornly low, even in the face of short-term inflation concerns. Tax policy is unlikely to change significantly over this year and next with our evenly divided Senate and all these pieces together create a very accommodative monetary and fiscal environment.

There are challenges too. Inflation could remain more persistent than economists suspect and erode some of the advantages of growth. Inflation has been very much on investors’ minds of late and, at some point, bond markets could react with higher interest rates, creating a headwind for the economy with increased costs for business and consumer purchases. There is still uncertainty about the trajectory of the virus and will be until most of the world’s population has been vaccinated. There is always plenty to worry about.

Times like these are excellent opportunities to review overall portfolio mix and contemplate the effect of volatility on our portfolios. While we don’t recommend trying to time the market, thinking about how our portfolio will react in the next downturn is a very useful exercise. Stocks are volatile, that is why we think of them as long-term investments. Over market cycles they tend to provide returns higher than those to be found in more conservative investments but over shorter periods their volatility can be discouraging to some. If we prepare for the inevitable downturn, we won’t be surprised when it appears, and that preparation will enable us to stick with our plan instead of allowing fear to precipitate costly mistakes.

Fortunately, we have a very recent example in the selloff of February and March of 2020. A quick review of your statements from that period will give a good idea of how your portfolio reacted then. Of course, not all downturns are alike, and the depth of the decline can vary. We’re certainly happy to discuss this with you at any time, just let us know.

In the meantime though, it’s summer, you can take your mask off (at least some of the time) and can enjoy those special times with family and friends that you may have had to put off for far too long. The economy is growing, and folks are going back to work. The sun is shining, and the birds are singing. How sweet it is!

We do not provide legal or tax advice. Reader should consult their own legal or tax advisor. There is no guarantee investment strategies will be successful. Investing involves risks, including possible loss of principal. There is always the risk that an investor may lose money. A long-term investment approach cannot guarantee a profit. Investors should talk to their financial advisor prior to making any investment decision. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

0 Comments