|

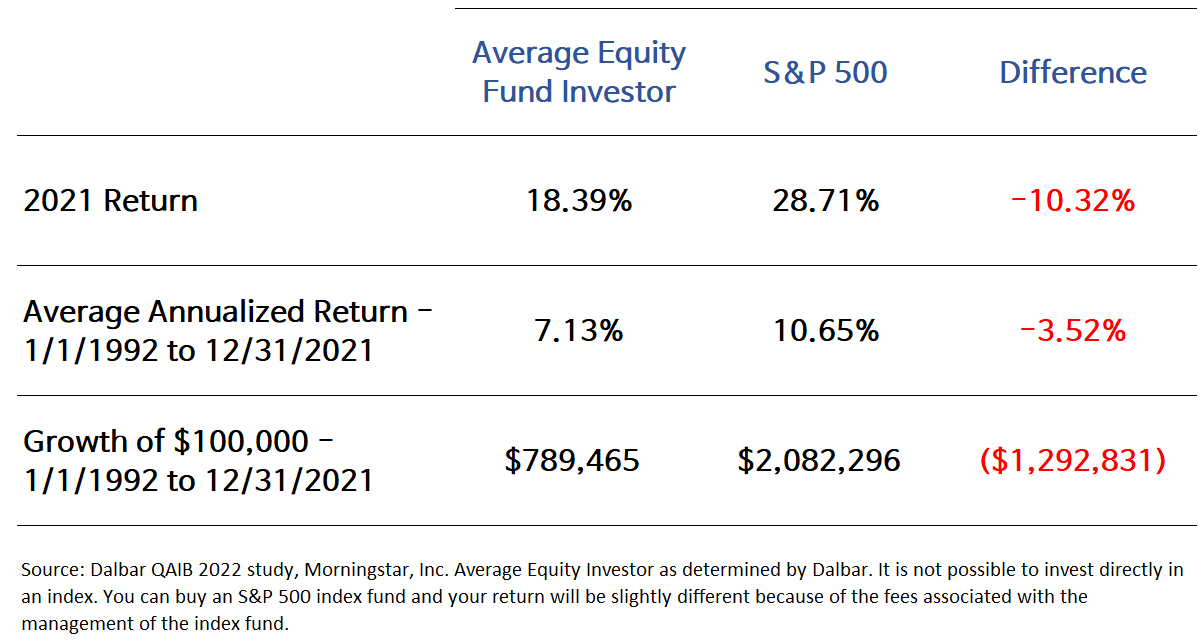

Warren Buffett, the Oracle of Omaha, once said to be fearful when others are greedy, and greedy when others are fearful.  You may have your money tied up in the stock market. Perhaps you went for the “shiny objects” and bought some popular high-tech company stocks and enjoyed watching your investments grow. But lately, you’ve been startled by the falling stock prices. You are tempted to sell your investments for much less than what you paid for them, exactly the opposite of Buffett's advice. I don’t blame you. That’s human nature. Who wouldn’t be tempted when you see others getting fabulously rich – sometimes very quickly – on Bitcoin and Tesla stock? Never mind that you don’t fully understand your investments. After all, isn’t that the whole point of investing? To sit back and enjoy your balance go up and up? But for long-term investment success, picking stocks based on past performance or trying to outguess the market is bound to fail. According to the annual Quantitative Analysis of Investor Behavior report by Dalbar, Inc., the S&P 500 returned 28.71% in 2021. The average investor? 18.39%. That’s a whopping 10% difference. Wait, it gets worse. Over 30 years, from 1/1/1992 to 12/31/2021, the S&P 500 returned 10.65% annually vs. average investor’s 7.13%. To put this in perspective, if you invested $100,000 in the S&P 500 on the first day of 1992, you would have ended up with $2,082,296 at the end of 2021. If you were an average investor earning 7.13%, your balance at 12/31/2021 would be $789,465. In summary, it looks something like this.  Why the large difference? Why is the investor return different from the investment return? One obvious reason is that investors make investment choices based on their emotions. They tend to make irrational investment choices out of fear or greed. Not surprisingly, studies have observed a close relationship between fund flows and market returns. That is, when stock prices move up, money flocks to mutual funds; conversely, you see an outflow of money from these funds when the markets tank. Of course, it goes without saying that this “buy high, sell low” investor behavior is completely irrational. But, sadly, it’s quite typical. Academics refer to this phenomenon as behavioral finance. It’s the study of investor behavior – the psychology and behavior that has to do with investors chasing “shiny objects,” seeing only what they want to see, hearing only what they want to hear, and making irrational investment decisions. Knowing this, is there an antidote to such irrational investor behavior? You can consider the following:

We do not provide legal or tax advice. Readers should consult their own legal or tax advisor. There is no guarantee investment strategies will be successful. Investing involves risks, including possible loss of principal. There is always the risk that an investor may lose money. A long-term investment approach cannot guarantee a profit. Investors should talk to their financial advisor prior to making any investment decision. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

Comments are closed.

|

|

Advisory services offered through CS Planning Corp, an SEC registered investment advisor.

Insurance products offered through Elliott Bay Insurance LLC. Form CRS, Privacy Policy, and Additional Disclosures. |