- Published on

If you are nearing 60, it’s a good idea to start thinking about Social Security benefits. Maybe you have a few decades to go before reaching 60, but your parents may be close to that milestone. If so, then read on. You’ll pick up a few ideas here. Your parents will be proud.

When it comes to Social Security benefits, one of the most important decisions to make is when to start taking your benefits. It’s easy if you know when you’ll die. But since no one knows, it can get a little tricky.

If you claim it too early at, say, age 62, you’ll get a head start. But then you’ll be locked into a lower benefit amount for the rest of your life. Conversely, you can wait and go for the higher benefit amount. But if you die before you collect enough benefit payments, you’ll be worse off than if you started at age 62.

So what to do? Let’s start by covering some basics.

Full Retirement Age

When you talk about Social Security, there’s one word that keeps coming up: Full Retirement Age, or FRA.

What is FRA? Quite simply, FRA is the age you are eligible to receive 100% of your Social Security benefit. You can think of it as the baseline age – as well as baseline benefit. By the way, the benefit paid at FRA is called Primary Insurance Amount, or PIA. PIA is another word you might hear frequently when discussing Social Security.

In the old days, FRA used to be 65. For today’s retirees, FRA is 66. If you’re born in 1960 or later, your FRA is 67. (For our discussion here, let’s go with age 66.)

If someone tells you your Social Security benefit is $1,000 at Full Retirement Age, it simply means that you’ll receive $1,000 at age 66.

Benefit Amount by Age

Now that we know what FRA is, you should also know that you can start your benefit earlier or later than your FRA. The earliest you can start is at age 62 and the latest is age 70. Between 62 and 70, you can choose any age to start your benefit.

So, why wouldn’t anyone start at 62? Said differently, why would anyone wait until 70?

It’s because the benefit amount is different based on when you start taking your benefit. If you start at 62, you will receive 25% less than if you waited until your FRA (age 66). On the other hand, if you wait until 70 to start your benefit, your monthly check will be 32% higher than if you began at FRA.

Here’s an example. Let’s say your benefit is $1,000 at FRA. At age 62, the benefit is 25% lower at $750. At age 70, it’s $1,320 because it’s 32% higher.

If you claim it too early at, say, age 62, you’ll get a head start. But then you’ll be locked into a lower benefit amount for the rest of your life. Conversely, you can wait and go for the higher benefit amount. But if you die before you collect enough benefit payments, you’ll be worse off than if you started at age 62.

So what to do? Let’s start by covering some basics.

Full Retirement Age

When you talk about Social Security, there’s one word that keeps coming up: Full Retirement Age, or FRA.

What is FRA? Quite simply, FRA is the age you are eligible to receive 100% of your Social Security benefit. You can think of it as the baseline age – as well as baseline benefit. By the way, the benefit paid at FRA is called Primary Insurance Amount, or PIA. PIA is another word you might hear frequently when discussing Social Security.

In the old days, FRA used to be 65. For today’s retirees, FRA is 66. If you’re born in 1960 or later, your FRA is 67. (For our discussion here, let’s go with age 66.)

If someone tells you your Social Security benefit is $1,000 at Full Retirement Age, it simply means that you’ll receive $1,000 at age 66.

Benefit Amount by Age

Now that we know what FRA is, you should also know that you can start your benefit earlier or later than your FRA. The earliest you can start is at age 62 and the latest is age 70. Between 62 and 70, you can choose any age to start your benefit.

So, why wouldn’t anyone start at 62? Said differently, why would anyone wait until 70?

It’s because the benefit amount is different based on when you start taking your benefit. If you start at 62, you will receive 25% less than if you waited until your FRA (age 66). On the other hand, if you wait until 70 to start your benefit, your monthly check will be 32% higher than if you began at FRA.

Here’s an example. Let’s say your benefit is $1,000 at FRA. At age 62, the benefit is 25% lower at $750. At age 70, it’s $1,320 because it’s 32% higher.

You should note that your benefit maxes out at age 70, so you gain nothing by waiting beyond age 70 to start your benefit.

Now, back to the question: When should you starting taking your Social Security benefit? There are at least 3 things you should consider.

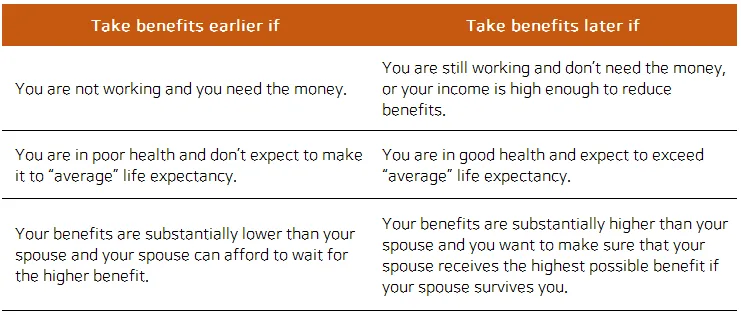

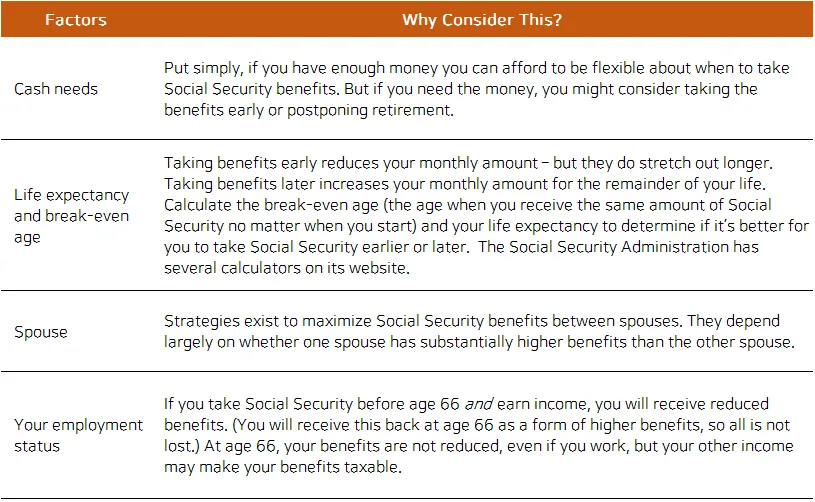

1. Life Expectancy

One obvious point is, if you’re healthy and can reasonably expect to live long, it would seem more advantageous to wait until 70. Conversely, if you’re in poor health and don’t expect to make it to “average” life expectancy, it’s probably best to consider starting at 62.

For reference, life expectancy in the U.S. for a 60-year old is 21.3 years for male and 24.4 years for female. That’s 81.3 for male and 84.4 for female. It’s only average for the entire U.S. population, so your own personal life expectancy can be very possibly much longer. Curiously, people with more education tend to live longer than those who are less educated. Married people also live longer than single people.

Now, back to the question: When should you starting taking your Social Security benefit? There are at least 3 things you should consider.

1. Life Expectancy

One obvious point is, if you’re healthy and can reasonably expect to live long, it would seem more advantageous to wait until 70. Conversely, if you’re in poor health and don’t expect to make it to “average” life expectancy, it’s probably best to consider starting at 62.

For reference, life expectancy in the U.S. for a 60-year old is 21.3 years for male and 24.4 years for female. That’s 81.3 for male and 84.4 for female. It’s only average for the entire U.S. population, so your own personal life expectancy can be very possibly much longer. Curiously, people with more education tend to live longer than those who are less educated. Married people also live longer than single people.

2. Cash Needs

Another consideration is cash needs. If you’re still working or you don’t need the money, you might consider waiting until 70. But if you need the money, well, you have little choice but to start taking your benefits.

3. Marital Status

Back in the day, there were some savvy planning opportunities for married couples, but they more or less disappeared in 2016 with the exception of a small group of people of certain ages who grandfathered in. Still, if you’re married, there still may be some planning opportunities especially if one of you has substantially higher benefits than the other. Curiously, these opportunities may apply to you even if you're divorced.

Another consideration is cash needs. If you’re still working or you don’t need the money, you might consider waiting until 70. But if you need the money, well, you have little choice but to start taking your benefits.

3. Marital Status

Back in the day, there were some savvy planning opportunities for married couples, but they more or less disappeared in 2016 with the exception of a small group of people of certain ages who grandfathered in. Still, if you’re married, there still may be some planning opportunities especially if one of you has substantially higher benefits than the other. Curiously, these opportunities may apply to you even if you're divorced.

We do not provide legal or tax advice. Reader should consult their own legal or tax advisor. There is no guarantee investment strategies will be successful. Investing involves risks, including possible loss of principal. There is always the risk that an investor may lose money. A long-term investment approach cannot guarantee a profit. Investors should talk to their financial advisor prior to making any investment decision. This information is intended for educational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

0 Comments